|

On the Affordable Health Care Act of 2010

And the Government Shutdown 09/30/2013 Updated 12/02/2016 |

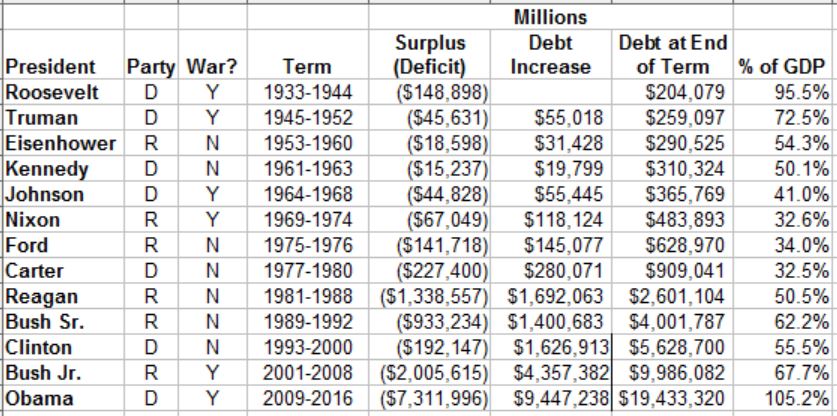

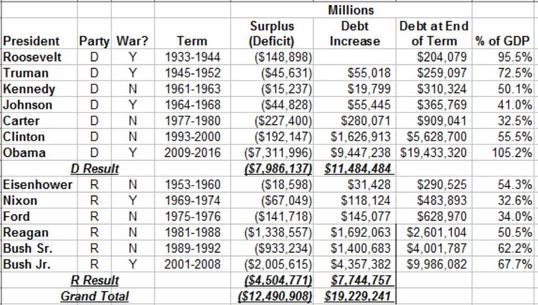

United States Deficits and Debt, by President & Party, 1933-2016

|

Observation: on the whole, but for Presidents Obama and Clinton, viewed through the lens of partisan presidencies (which is hotly debated but probably over-simplified), insofar as they've borrowed less, Democrats have proven to be better stewards than Republicans. While the Democrat total is caused almost entirely by one President (Obama), the Republican total is mostly caused by three: Reagan, and both Bushes.

Questions:

|

On the Affordable Health Care Act of 2010. Since the daily news is focused on the A.H.A. and the pending government shutdown, as I read of falling markets and am ever mindful that the best time to buy is when everyone else is selling, and that crises often contain hidden opportunities noticeable to astute observers, I decided to take a quick look at what's happening in the mutual fund market right now, relate it to current news, and share my findings and observations.

What IS the A.H.A.? As far as I can tell at the moment, it is more of a theory than a reality. Since it presupposes and depends on widespread cooperation in the health care industry, the reality of it has yet to be worked out; and according to a recent piece I read in the Wall Street Journal, information system software design will be a major hurdle in achieving this cooperation. Indeed, it will probably be THE bottleneck in realizing the theory.

So what is the current reality? Firstly, if you are worried about affording increasing premia, once you've learned what your new premium may be from the myriad what-if calculators out there, I encourage you to work out your whole household budget and track it properly so you can really know not just the cost of your health insurance, but the cost of your life. If you find the challenge too daunting, I'm here to help. Indeed, I'd suggest taking it a step further, looking not just at this year's expenses, but thinking long-term by developing a Lifetime Savings Plan. You can do it right here free of charge.

As an outcome of both long and short term planning, you will probably discover that, like so many, you need to improve your income. But the difference is, you'll know how much is enough. It will no longer be a vague sense that more money would be nice; it will be an absolute certainty about how much more income is enough, a goal that you can pursue with a clear conscience, knowing that you're not being greedy; you're being responsible.

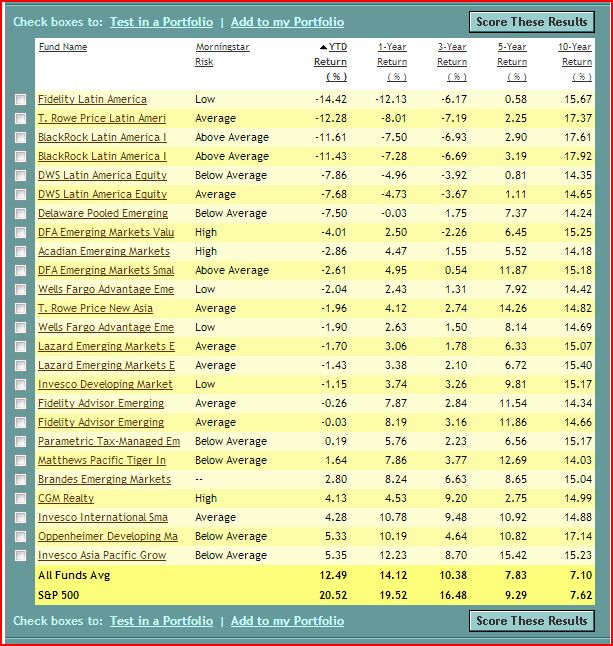

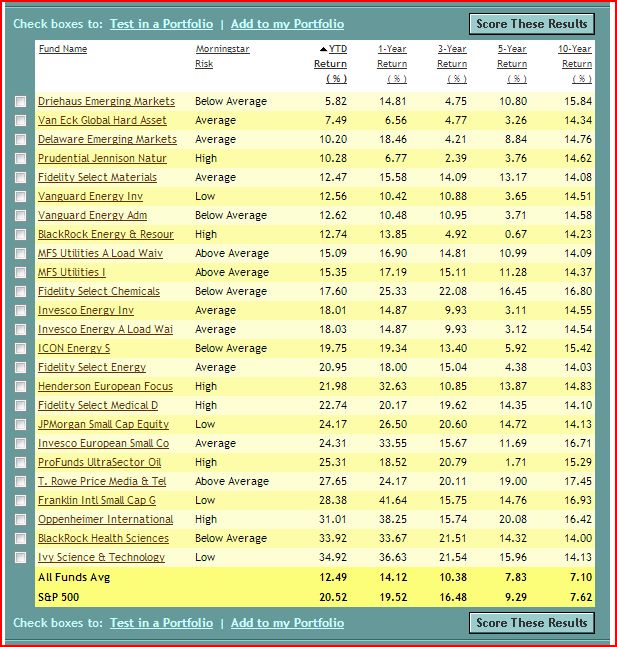

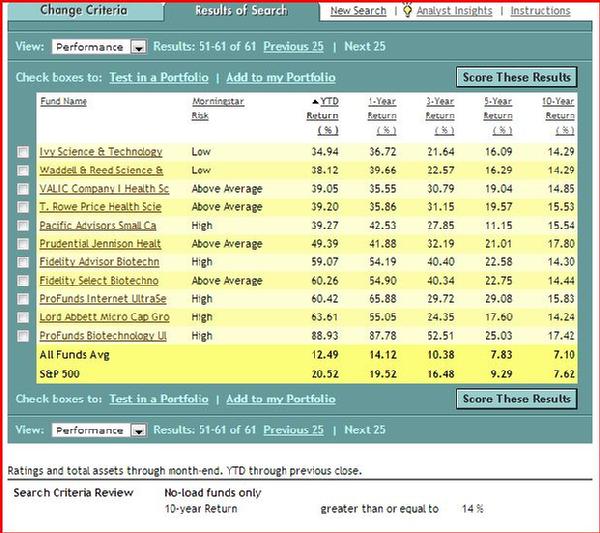

Secondly, in my attempt to answer the question, I used Morningstar's mutual fund screener, which I also use to prepare my annual investment report, to sort no-load funds with a ten year average annual return better than 14% by year-to-date return from low to high. I was curious to know where the bargains are among funds that have a long-term history of excellent performance, whether the current news about the A.H.A. and the pending government shutdown was affecting them, and if so, how. The results of this search are in the three below screen shots:

What IS the A.H.A.? As far as I can tell at the moment, it is more of a theory than a reality. Since it presupposes and depends on widespread cooperation in the health care industry, the reality of it has yet to be worked out; and according to a recent piece I read in the Wall Street Journal, information system software design will be a major hurdle in achieving this cooperation. Indeed, it will probably be THE bottleneck in realizing the theory.

So what is the current reality? Firstly, if you are worried about affording increasing premia, once you've learned what your new premium may be from the myriad what-if calculators out there, I encourage you to work out your whole household budget and track it properly so you can really know not just the cost of your health insurance, but the cost of your life. If you find the challenge too daunting, I'm here to help. Indeed, I'd suggest taking it a step further, looking not just at this year's expenses, but thinking long-term by developing a Lifetime Savings Plan. You can do it right here free of charge.

As an outcome of both long and short term planning, you will probably discover that, like so many, you need to improve your income. But the difference is, you'll know how much is enough. It will no longer be a vague sense that more money would be nice; it will be an absolute certainty about how much more income is enough, a goal that you can pursue with a clear conscience, knowing that you're not being greedy; you're being responsible.

Secondly, in my attempt to answer the question, I used Morningstar's mutual fund screener, which I also use to prepare my annual investment report, to sort no-load funds with a ten year average annual return better than 14% by year-to-date return from low to high. I was curious to know where the bargains are among funds that have a long-term history of excellent performance, whether the current news about the A.H.A. and the pending government shutdown was affecting them, and if so, how. The results of this search are in the three below screen shots:

Private sector leaders opine that the A.H.A. is not sustainable and will die a natural death. Since the private sector drives everything else, I have to respect their opinions.

Presuming they're right, as we go through the national experience of attempting it, encountering these obstacles and bottlenecks, discovering that they're right, and experiencing and learning from our mistakes, where are the hidden opportunities in what otherwise appears to be a crisis?

As I scan the above results, I notice foreign investment funds starting with Latin America on the first page, energy and tangible assets on the second, and the health care industry near the end with highest current returns; and I ask myself what, if any, effect news about the current situation has had on these.

As far as timing of investment is concerned, I've noticed two schools of thought: 1) Catch a rising star, and 2) buy low, sell high. The down-sides of each are 1) Performance-chasing, and 2) Catching a falling knife. To counter the down-side, we need to look beneath the numbers by doing our homework and thinking things through.

I don't know whether our current domestic situation has any relationship with the results of the foreign investments on the first page. Regardless, their current positions present bargain opportunities and havens from domestic difficulties. Buy low, sell high.

The relationship between the A.H.A. and the high returns enjoyed by investors in the health care industry is obvious to me: there is much work to be done in the industry to deal with it - whether that work is to implement it, or to recover from its failure and devise a better solution. Regardless, investors in health care have been winning for quite some time; and I suspect they will keep winning for the foreseeable future as baby boomers continue to need and demand the best care, and as they either benefit or learn from the A.H.A. experience.

As I review the 1996-2013 Sector Analysis that I include in each Annual Report, I notice that Health Care appeared in 1996, 1998, 2001, 2011, and this year. I am wondering aloud with you whether concern about the A.H.A. will continue to contribute, perhaps indirectly, to the excellent returns that investors in the industry have been enjoying for the past decade.

I will not go so far as to make a buy or sell recommendation; I don't have the credentials to do that. But I thought you might appreciate having these findings, which you can share with those who are credentialed to make such recommendations, as you continue to evaluate your own investment options.

One thing I CAN do is help you know how much you need to invest to afford the life you want, and know your real Return on Investment so that you can compare it with your goal and make sure you're on track. I share this investment research to help you shorten your learning curve, and get an objective, impartial, independent definition of excellence.

For more assistance like this, please contact me.

On the Government Shutdown. First of all, if your income is interrupted because of the government shutdown, if you haven't yet, consider this incident a gentle nudge to develop an Emergency Fund, which should be between three and twelve months' living expenses. The Emergency Fund is Goal #1 on the Lifetime Savings Plan. In my research I have discovered that on average over a lifetime, it is fair and reasonable to expect an emergency of such a magnitude to happen once every four years. To develop your Emergency Fund, go through the Lifetime Savings Plan questionnaire, or if that is too complicated, just contact me and I'll help you out.

Although they sound alarming, over the years I have learned that government shutdowns are neither dire nor permanent. They are temporary political devices that alarm the public and create political pressure intended to force differing groups to compromise and agree. They're driven by the country's debt, and are resolved when the differing parties agree on a new debt limit.

To many of us, it seems more like show than substance, Shakespeare's "sound and fury, signifying nothing," a mere wolf-crying exercise. Politicians cry wolf, there's a brief cash flow hiccup for some government employees, then before we know it it's business as usual, and we stop thinking about it until the next time.

But there is an important economic reality underlying all of this fuss about which I've found that many otherwise very smart people are confused. For example, I have met Ph.D. level intellectuals who do not understand the difference between "Deficit" and "Debt." They understand that they're both economically bad things that begin with the letter "D" but beyond that, they can not explain the difference clearly and, more often than not, get lost in endless wrangling about partisan politics, and when I try to discuss it with them their eyes glaze over and they change the subject.

Be that as it may, here is some clarity I'm offering to anyone with eyes to see:

A Deficit is the excess of expenses over income in a finite time period, usually a year. (Its opposite is a surplus, the excess of income over expenses.)

Debt occurs when cumulative deficits exceed cumulative surpluses since the beginning. It is the sum of all deficits, all surpluses, and interest.

Here is the history of the United States' surpluses and deficits since 1789. As you can see, the greatest times of deficit happened during times of war, which are bi-partisan decisions (Whitehouse.gov, Table 1.1).

Here is the history of the United States' debt since 1940. As the nation and its economy grows, the debt figures become mind-blowing. But here are a couple of important things to understand: 1) The country has always been in debt. 2) What really matters is the proportion of debt to Gross Domestic Product (GDP). As you can see, our 2012 proportion was 103.2%. The highest it has ever been is 121.7% in 1946, when we were in the middle of World War Two (Whitehouse.gov, Table 7.1).

But we recovered after the war and drove the proportion down as low as 33.2% in 1979. Since then, through several administrations, both liberal and conservative, we've grown that proportion again to where it is now.

I am convinced that, just as we did before, we can, and we will, drive the percentage back down. Furthermore, I am convinced that by producing consistent surpluses, we can eliminate the debt entirely. It may happen in my grandchildren's or great grandchildren's generations, but I am convinced it's possible.

That is the Vision and purpose of Making End$ Meet: by working one household and one business at a time, to help people thrive, produce surpluses, fully fund their futures, become more self-sufficient and less reliant on government entitlements, contribute to the government's surplus so that it can pay off its debts, and otherwise be not part of the problem, but part of the solution.

Please let me help you and yours work toward that end.

For your happiness and success in all things,

Kris Freeberg, Economist

Making End$ Meet

[email protected]

(360) 224-4322

Presuming they're right, as we go through the national experience of attempting it, encountering these obstacles and bottlenecks, discovering that they're right, and experiencing and learning from our mistakes, where are the hidden opportunities in what otherwise appears to be a crisis?

As I scan the above results, I notice foreign investment funds starting with Latin America on the first page, energy and tangible assets on the second, and the health care industry near the end with highest current returns; and I ask myself what, if any, effect news about the current situation has had on these.

As far as timing of investment is concerned, I've noticed two schools of thought: 1) Catch a rising star, and 2) buy low, sell high. The down-sides of each are 1) Performance-chasing, and 2) Catching a falling knife. To counter the down-side, we need to look beneath the numbers by doing our homework and thinking things through.

I don't know whether our current domestic situation has any relationship with the results of the foreign investments on the first page. Regardless, their current positions present bargain opportunities and havens from domestic difficulties. Buy low, sell high.

The relationship between the A.H.A. and the high returns enjoyed by investors in the health care industry is obvious to me: there is much work to be done in the industry to deal with it - whether that work is to implement it, or to recover from its failure and devise a better solution. Regardless, investors in health care have been winning for quite some time; and I suspect they will keep winning for the foreseeable future as baby boomers continue to need and demand the best care, and as they either benefit or learn from the A.H.A. experience.

As I review the 1996-2013 Sector Analysis that I include in each Annual Report, I notice that Health Care appeared in 1996, 1998, 2001, 2011, and this year. I am wondering aloud with you whether concern about the A.H.A. will continue to contribute, perhaps indirectly, to the excellent returns that investors in the industry have been enjoying for the past decade.

I will not go so far as to make a buy or sell recommendation; I don't have the credentials to do that. But I thought you might appreciate having these findings, which you can share with those who are credentialed to make such recommendations, as you continue to evaluate your own investment options.

One thing I CAN do is help you know how much you need to invest to afford the life you want, and know your real Return on Investment so that you can compare it with your goal and make sure you're on track. I share this investment research to help you shorten your learning curve, and get an objective, impartial, independent definition of excellence.

For more assistance like this, please contact me.

On the Government Shutdown. First of all, if your income is interrupted because of the government shutdown, if you haven't yet, consider this incident a gentle nudge to develop an Emergency Fund, which should be between three and twelve months' living expenses. The Emergency Fund is Goal #1 on the Lifetime Savings Plan. In my research I have discovered that on average over a lifetime, it is fair and reasonable to expect an emergency of such a magnitude to happen once every four years. To develop your Emergency Fund, go through the Lifetime Savings Plan questionnaire, or if that is too complicated, just contact me and I'll help you out.

Although they sound alarming, over the years I have learned that government shutdowns are neither dire nor permanent. They are temporary political devices that alarm the public and create political pressure intended to force differing groups to compromise and agree. They're driven by the country's debt, and are resolved when the differing parties agree on a new debt limit.

To many of us, it seems more like show than substance, Shakespeare's "sound and fury, signifying nothing," a mere wolf-crying exercise. Politicians cry wolf, there's a brief cash flow hiccup for some government employees, then before we know it it's business as usual, and we stop thinking about it until the next time.

But there is an important economic reality underlying all of this fuss about which I've found that many otherwise very smart people are confused. For example, I have met Ph.D. level intellectuals who do not understand the difference between "Deficit" and "Debt." They understand that they're both economically bad things that begin with the letter "D" but beyond that, they can not explain the difference clearly and, more often than not, get lost in endless wrangling about partisan politics, and when I try to discuss it with them their eyes glaze over and they change the subject.

Be that as it may, here is some clarity I'm offering to anyone with eyes to see:

A Deficit is the excess of expenses over income in a finite time period, usually a year. (Its opposite is a surplus, the excess of income over expenses.)

Debt occurs when cumulative deficits exceed cumulative surpluses since the beginning. It is the sum of all deficits, all surpluses, and interest.

Here is the history of the United States' surpluses and deficits since 1789. As you can see, the greatest times of deficit happened during times of war, which are bi-partisan decisions (Whitehouse.gov, Table 1.1).

Here is the history of the United States' debt since 1940. As the nation and its economy grows, the debt figures become mind-blowing. But here are a couple of important things to understand: 1) The country has always been in debt. 2) What really matters is the proportion of debt to Gross Domestic Product (GDP). As you can see, our 2012 proportion was 103.2%. The highest it has ever been is 121.7% in 1946, when we were in the middle of World War Two (Whitehouse.gov, Table 7.1).

But we recovered after the war and drove the proportion down as low as 33.2% in 1979. Since then, through several administrations, both liberal and conservative, we've grown that proportion again to where it is now.

I am convinced that, just as we did before, we can, and we will, drive the percentage back down. Furthermore, I am convinced that by producing consistent surpluses, we can eliminate the debt entirely. It may happen in my grandchildren's or great grandchildren's generations, but I am convinced it's possible.

That is the Vision and purpose of Making End$ Meet: by working one household and one business at a time, to help people thrive, produce surpluses, fully fund their futures, become more self-sufficient and less reliant on government entitlements, contribute to the government's surplus so that it can pay off its debts, and otherwise be not part of the problem, but part of the solution.

Please let me help you and yours work toward that end.

For your happiness and success in all things,

Kris Freeberg, Economist

Making End$ Meet

[email protected]

(360) 224-4322