A Little Budgeting Poem

August, 2015 I've looked around; The myths persist. The average month Does not exist. |

short-term savingsLet Us Celebrate!

More Joy, Less Stress: How to Prepare for Irregular Expenses September 18, 2014 |

Holidays should be joyful.

Without the stress of borrowing, here's how to prepare for them, and many other similar irregular expenses.

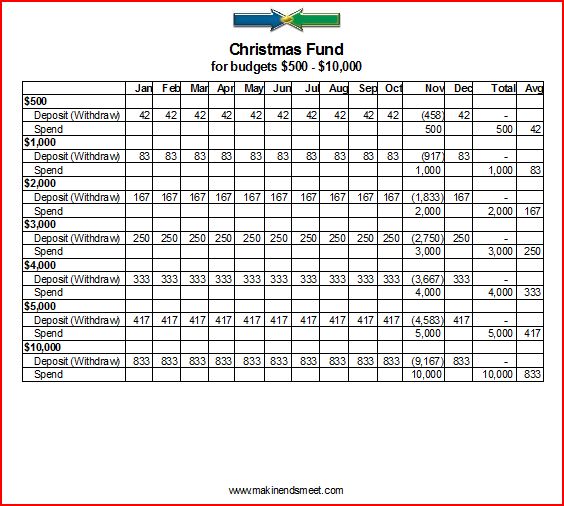

From above, suppose we wanted a $2,000 Christmas Fund,

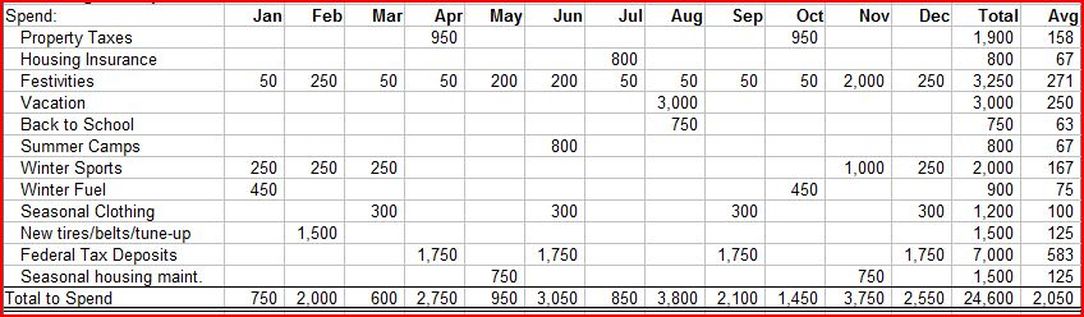

In addition, suppose we also wanted $200 for things like Valentine's Day, Mother's Day, Father's Day, and New Year's Day, and a slush fund of $50 per month for unplanned occasions like friends' birthday parties, baby showers, anniversaries, and so forth. Altogether, let's call them "Festivities", totaling $3,250 for the year and averaging $271 per month.

Beside that, there are other irregular expenses to consider:

In addition, suppose we also wanted $200 for things like Valentine's Day, Mother's Day, Father's Day, and New Year's Day, and a slush fund of $50 per month for unplanned occasions like friends' birthday parties, baby showers, anniversaries, and so forth. Altogether, let's call them "Festivities", totaling $3,250 for the year and averaging $271 per month.

Beside that, there are other irregular expenses to consider:

Irregular Expense Budget, or Spending Plan

Unforeseen, they can seem pretty disruptive, ranging from as little as $600 in March to as much as $3,800 in August. Their annual total is $24,600, averaging $2,050 per month. Unforeseen, they'd seem like surprises and one might either fail to afford them and do without, or borrow. Foreseen, they can be afforded through adequate earning.

Each month is so different, which is why budget techniques that confine their scope to monthly averages are so discouraging and lame. How shall one manage that income to afford things when they're due?

The ordinary way is to borrow; kick the can down the road; spend now, pay later, which is definitely lame, and most definitely NOT awesome. By adding interest to the equation, it's the most expensive option, sometimes resulting ultimately in train wrecks like bankruptcy and worse.

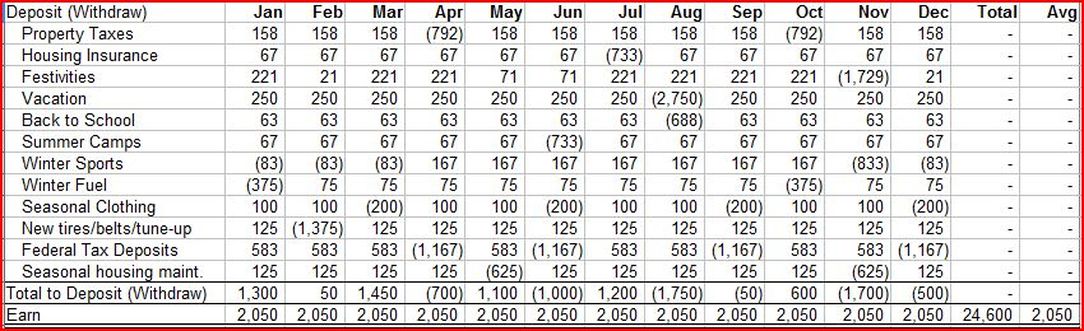

The least expensive, most joyful way is to receive interest instead of paying it by saving instead of borrowing. Let interest, dividend, and capital gain income help pay for these expenses. Don't treat them as though they were surprises; they're not. They're perfectly predictable, and working with the above monthly averages, we can prepare for them like this:

Each month is so different, which is why budget techniques that confine their scope to monthly averages are so discouraging and lame. How shall one manage that income to afford things when they're due?

The ordinary way is to borrow; kick the can down the road; spend now, pay later, which is definitely lame, and most definitely NOT awesome. By adding interest to the equation, it's the most expensive option, sometimes resulting ultimately in train wrecks like bankruptcy and worse.

The least expensive, most joyful way is to receive interest instead of paying it by saving instead of borrowing. Let interest, dividend, and capital gain income help pay for these expenses. Don't treat them as though they were surprises; they're not. They're perfectly predictable, and working with the above monthly averages, we can prepare for them like this:

Short-Term Savings Plan to Manage Irregular Expenses

As you can see, with good foresight, we determined that to afford these expenses, we needed to earn $2,050 per month, and manage these earnings by following the above short-term savings plan. With it, instead of thinking about and managing these expenses one by one, we summarize them into single monthly deposits and withdrawals.

Now, having worked it out, we can shift our focus from futility to triumph: from juggling acts, compromises, can-kicking, "robbing Peter to pay Paul", stressful consumer debt, and otherwise "rearranging deck chairs on the Titanic", to earning the $24,600 with a clear mind and a whole heart, and managing it well.

This is winning. This is what it's like to be awesome.

For help including irregular expenses in your budget, improving your income to afford them, or otherwise being awesome, please contact us.

Now, having worked it out, we can shift our focus from futility to triumph: from juggling acts, compromises, can-kicking, "robbing Peter to pay Paul", stressful consumer debt, and otherwise "rearranging deck chairs on the Titanic", to earning the $24,600 with a clear mind and a whole heart, and managing it well.

This is winning. This is what it's like to be awesome.

For help including irregular expenses in your budget, improving your income to afford them, or otherwise being awesome, please contact us.

Click image for a clearer, printer-ready, PDF format version of this plan.