|

Book Review

Simple Numbers, Straight Talk, Big Profits! by Greg Crabtree Published 2011 Reviewed July 2019 |

Click for author's web site

Reading this book changed how I work and operate my practice.

I learned about it while listening to podcasts about running property management companies. In particular, I recall my colleague Danny Craig dropping Crabtree's name and emphasizing the importance of Labor Efficiency. Others also mentioned Crabtree and his book. In view of this convergence of esteem, this consensus, I decided I had to have a read.

Let me preface this review by restating that I studied Managerial Accounting at the University of Washington under a master: Gary L. Sundem, author of the course text. Let me tell you, it is a rare treat to learn from the author of the text. From Gary I learned about the nuances of Contribution Margin and have used this intelligence in my work, hard-wiring it into the applications I develop.

Be that as it may, Crabtree opened my eyes to things they never thought to address at the UW back in the day when I took the course.

I learned about it while listening to podcasts about running property management companies. In particular, I recall my colleague Danny Craig dropping Crabtree's name and emphasizing the importance of Labor Efficiency. Others also mentioned Crabtree and his book. In view of this convergence of esteem, this consensus, I decided I had to have a read.

Let me preface this review by restating that I studied Managerial Accounting at the University of Washington under a master: Gary L. Sundem, author of the course text. Let me tell you, it is a rare treat to learn from the author of the text. From Gary I learned about the nuances of Contribution Margin and have used this intelligence in my work, hard-wiring it into the applications I develop.

Be that as it may, Crabtree opened my eyes to things they never thought to address at the UW back in the day when I took the course.

Here are my big take-aways:

One: Owner Salary. Believe it or not, business owners typically under-pay themselves. I'm sure this happens because founders build their businesses from nothing, get used to sacrificing for the business, and never get around to breaking the Sacrifice Habit even when they can afford to.

One client of mine calls this "Sergeant Major Syndrome" or eating last, only after all of the troops have eaten. The popular figure in 2011 when Crabtree wrote the book was $30,000 for somebody doing a $150,000 job.

When this happens, the company's profit is exaggerated by the owner's paltry salary, rendering their financial statements meaningless for comparison or ROI determination purposes, or even for the purpose of self-understanding.

Crabtree's advice is for owners to pay themselves a full market based salary and stop gaming profits and distributions. Then their profit margin will actually mean something.

Doing this may reveal that the business' income function is broken. If so, the opportunity is exposed to fix it.

But as long as owners continue fooling and under-paying themselves, the broken income function will remain obscured, and owners will delude themselves into thinking that their businesses are doing better than they really are.

Two: Getting Serious about Taxes. Crabtree asserts that a 10% profit margin is "the new break even" because on an as-you-go basis, profit appearing on financial statements is pre-tax. If you're making less than ten percent, you don't have enough profit to afford taxes.

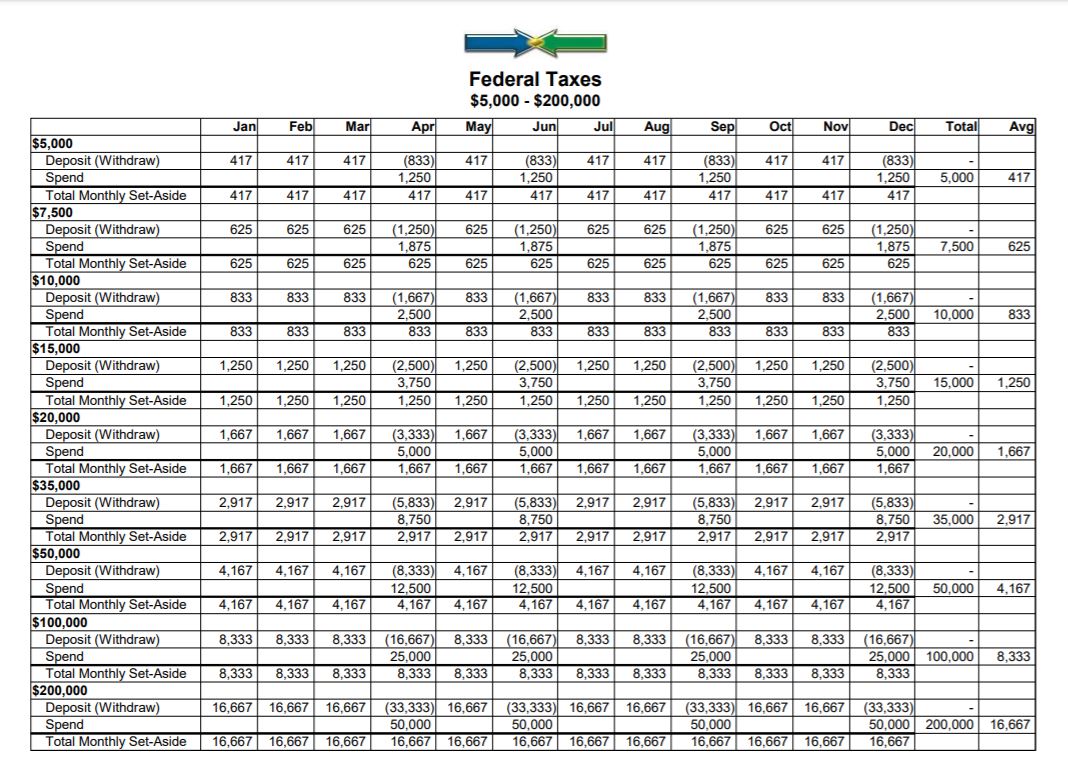

Furthermore - and this flabbergasted me - Crabtree asserts that "Almost every entrepreneur . . . is confused about whether the company's taxes are coming from this year's profits or last year's profits" (74). Learning this prompted me to formalize the following chart, which until now has been a part of the Short Term Savings Plans in the Budgets that I write. Because of Crabtree, I decided to make this a stand-alone document, a kind of Flexible Tax Savings Plan:

One: Owner Salary. Believe it or not, business owners typically under-pay themselves. I'm sure this happens because founders build their businesses from nothing, get used to sacrificing for the business, and never get around to breaking the Sacrifice Habit even when they can afford to.

One client of mine calls this "Sergeant Major Syndrome" or eating last, only after all of the troops have eaten. The popular figure in 2011 when Crabtree wrote the book was $30,000 for somebody doing a $150,000 job.

When this happens, the company's profit is exaggerated by the owner's paltry salary, rendering their financial statements meaningless for comparison or ROI determination purposes, or even for the purpose of self-understanding.

Crabtree's advice is for owners to pay themselves a full market based salary and stop gaming profits and distributions. Then their profit margin will actually mean something.

Doing this may reveal that the business' income function is broken. If so, the opportunity is exposed to fix it.

But as long as owners continue fooling and under-paying themselves, the broken income function will remain obscured, and owners will delude themselves into thinking that their businesses are doing better than they really are.

Two: Getting Serious about Taxes. Crabtree asserts that a 10% profit margin is "the new break even" because on an as-you-go basis, profit appearing on financial statements is pre-tax. If you're making less than ten percent, you don't have enough profit to afford taxes.

Furthermore - and this flabbergasted me - Crabtree asserts that "Almost every entrepreneur . . . is confused about whether the company's taxes are coming from this year's profits or last year's profits" (74). Learning this prompted me to formalize the following chart, which until now has been a part of the Short Term Savings Plans in the Budgets that I write. Because of Crabtree, I decided to make this a stand-alone document, a kind of Flexible Tax Savings Plan:

Click for a printer-ready PDF version

The idea here is, at the BEGINNING of each year, reckon what that year's taxes might be, set aside funds monthly, then make Federal Tax Deposits (FTDs) quarterly. For example if you reckon your taxes will be in the $20,000 realm, set aside $1,667 a month in the months quarterly payments are not due, and withdraw $3,333 in the months when they are due to afford the $5,000 quarterly payments. The remaining $1,667 comes from that month's income. In this way we regulate an irregular thing, translating the $5,000 quarterly burden into a routine $1,667 monthly transaction.

Do NOT wait until April 15 of the following year (or worse, October if you file an extension) to begin thinking about how to afford your taxes. Manage for taxes in the year they are incurred, from that year's profits.

It seems like common sense, doesn't it? But accordingly to Crabtree, almost nobody is doing it.

Astounding!

Learning this got me thinking very deeply about what Patriotism is. Some people are patriotic because they are federal employees or in the military, receiving wages and pensions from the government. Of course they would be patriotic: look who's buttering their bread!

But I came to realize that a true test of patriotism is whether, and how, one pays one's taxes. A true patriot is on top of his or her tax game. True patriots file promptly and accurately, they report the full amount that they owe, and they pay it promptly. A true patriot files their 1040 early and shows a big fat zero at the bottom of the return because they made their quarterly deposits on time and in full.

Imagine how different things would be if most citizens did this. What effect do you suppose this One Thing would have on the national debt, and on the country's fiscal and military strength?

Three: The Salary Cap. The idea here is if you know roughly what your annual revenue will be and you know your non-salary costs, then it's possible to set an overall salary cap that will ensure your necessary profit margin. In the example he gave, if you know your revenue will be around $1M and your non-salary costs are $400K and you need a 10% profit margin or $100K, then your salary cap must be $500K.

So you say to yourself, "$500K is my labor budget. What would be the wisest way to spend it?"

In this way you suss out your rock stars, eliminate the slackers, and make your business thrive. Otherwise you succumb to Labor Creep, operating at Break Even or worse while the slackers abuse you and, exasperated by them, the rock stars leave.

Regardless what games or gimmicks you play with compensation - salary, hourly, commissions, profit or margin sharing, bonuses, whatever - your cap is five hundred grand. PERIOD.

And that's ALL labor costs, not just salaries and wages: taxes, benefits, everything. They all count against the 100%.

Four: The Core Capital Target. This is so simple, so common sense, so brilliant.

The Core Capital Target is two months' operating expenses in cash, and no debt. Accumulate that before you take any significant distributions, and your business will thrive.

Cash is king, and magical miraculous opportunities come to those who have it.

Use that to define your "New Broke", your "New Zero." When your cash balance dips below two month's operating expenses, you're officially broke. At that point, do what you'd normally do if it were zero, like trim expenses and grow income. It's your New Zero.

I love this concept, I've been preaching it for years, but Crabtree helped me formalize, quantify, and name it.

Five: Labor Efficiency. Labor Efficiency is Gross Profit divided by Total Labor. It's a factor. If your Gross Profit were $1M and your Total Labor were $500K, your Labor Efficiency would be 2.0. The more efficient your labor is, the higher this factor will be.

This is so beautifully simple. It cuts through the distinctions between salaries, wages, benefits, taxes, production versus administration. Crabtree points out how administrative labor contributes to revenue by liberating production labor to produce. If the admin folks weren't there doing their admin things, the production folks would have to divide their attention and wouldn't be as focused and productive.

So it all contributes to revenue. It all matters. The thing to focus on is that single factor, and monitor it ongoingly.

Because we can, we who design payroll and accounting systems have a tendency to segment, to dissemble. We put production labor over here, and administration over there. This practice tends to obscure the labor picture. Crabtree says, sum it all, divide Gross Profit by it, and watch that factor like a hawk. Do everything you can think of to improve it.

Simple. Brilliant. Game-changing.

Six: The Rolling Twelve P&L. Look at this list:

Do you see the progression? Each is a twelve month period, one a month later than the other.

Now imagine a Profit and Loss statement with those as columns. That is the Rolling Twelve P&L and it is brilliant because it rises above seasonality variations and shows in annualized terms how your business is progressing.

Simple. Brilliant.

QuickBooks won't do it for you; I don't know of any accounting software that will. You have to spreadsheet it.

But it's easy. It takes less than an hour to compile a P&L showing twelve twelve month periods.

Game changer.

Seven: "Skip the budget. Learn to forecast."

Wow. I've been writing budgets over my whole career. Now this guy says they're not important?

Dang. He's right. I do forecasts too and I must say, if I had to choose between budgets and forecasts, if I had to say which is more important, I'd say it's the forecast. Of course I see a relationship between budgets and forecasts. In a sense the forecast predicts the cash flow effects of the budget, including expected revenue.

But in his down home Huntsville Alabama way, he draws a sharper distinction, putting it like this: "A budget is a license to spend. A forecast is your roadmap to profitability."

There have been times when my clients didn't have budgets. I could never get them to sit down and finish one with me. Whenever that has happened I've done what he recommends: forecast into the future working with recent actuals.

No budget necessary. It's Lean. It works.

Eight: The Crabtree KPIs (Key Performance Indicators):

Do NOT wait until April 15 of the following year (or worse, October if you file an extension) to begin thinking about how to afford your taxes. Manage for taxes in the year they are incurred, from that year's profits.

It seems like common sense, doesn't it? But accordingly to Crabtree, almost nobody is doing it.

Astounding!

Learning this got me thinking very deeply about what Patriotism is. Some people are patriotic because they are federal employees or in the military, receiving wages and pensions from the government. Of course they would be patriotic: look who's buttering their bread!

But I came to realize that a true test of patriotism is whether, and how, one pays one's taxes. A true patriot is on top of his or her tax game. True patriots file promptly and accurately, they report the full amount that they owe, and they pay it promptly. A true patriot files their 1040 early and shows a big fat zero at the bottom of the return because they made their quarterly deposits on time and in full.

Imagine how different things would be if most citizens did this. What effect do you suppose this One Thing would have on the national debt, and on the country's fiscal and military strength?

Three: The Salary Cap. The idea here is if you know roughly what your annual revenue will be and you know your non-salary costs, then it's possible to set an overall salary cap that will ensure your necessary profit margin. In the example he gave, if you know your revenue will be around $1M and your non-salary costs are $400K and you need a 10% profit margin or $100K, then your salary cap must be $500K.

So you say to yourself, "$500K is my labor budget. What would be the wisest way to spend it?"

In this way you suss out your rock stars, eliminate the slackers, and make your business thrive. Otherwise you succumb to Labor Creep, operating at Break Even or worse while the slackers abuse you and, exasperated by them, the rock stars leave.

Regardless what games or gimmicks you play with compensation - salary, hourly, commissions, profit or margin sharing, bonuses, whatever - your cap is five hundred grand. PERIOD.

And that's ALL labor costs, not just salaries and wages: taxes, benefits, everything. They all count against the 100%.

Four: The Core Capital Target. This is so simple, so common sense, so brilliant.

The Core Capital Target is two months' operating expenses in cash, and no debt. Accumulate that before you take any significant distributions, and your business will thrive.

Cash is king, and magical miraculous opportunities come to those who have it.

Use that to define your "New Broke", your "New Zero." When your cash balance dips below two month's operating expenses, you're officially broke. At that point, do what you'd normally do if it were zero, like trim expenses and grow income. It's your New Zero.

I love this concept, I've been preaching it for years, but Crabtree helped me formalize, quantify, and name it.

Five: Labor Efficiency. Labor Efficiency is Gross Profit divided by Total Labor. It's a factor. If your Gross Profit were $1M and your Total Labor were $500K, your Labor Efficiency would be 2.0. The more efficient your labor is, the higher this factor will be.

This is so beautifully simple. It cuts through the distinctions between salaries, wages, benefits, taxes, production versus administration. Crabtree points out how administrative labor contributes to revenue by liberating production labor to produce. If the admin folks weren't there doing their admin things, the production folks would have to divide their attention and wouldn't be as focused and productive.

So it all contributes to revenue. It all matters. The thing to focus on is that single factor, and monitor it ongoingly.

Because we can, we who design payroll and accounting systems have a tendency to segment, to dissemble. We put production labor over here, and administration over there. This practice tends to obscure the labor picture. Crabtree says, sum it all, divide Gross Profit by it, and watch that factor like a hawk. Do everything you can think of to improve it.

Simple. Brilliant. Game-changing.

Six: The Rolling Twelve P&L. Look at this list:

- Jan 2018 - Dec 2018

- Feb 2018 - Jan 2019

- Mar 2018 - Feb 2019

- Apr 2018 - Mar 2019

- May 2018 - Apr 2019

- Jun 2018 - May 2019

- Jul 2018 - Jun 2019

Do you see the progression? Each is a twelve month period, one a month later than the other.

Now imagine a Profit and Loss statement with those as columns. That is the Rolling Twelve P&L and it is brilliant because it rises above seasonality variations and shows in annualized terms how your business is progressing.

Simple. Brilliant.

QuickBooks won't do it for you; I don't know of any accounting software that will. You have to spreadsheet it.

But it's easy. It takes less than an hour to compile a P&L showing twelve twelve month periods.

Game changer.

Seven: "Skip the budget. Learn to forecast."

Wow. I've been writing budgets over my whole career. Now this guy says they're not important?

Dang. He's right. I do forecasts too and I must say, if I had to choose between budgets and forecasts, if I had to say which is more important, I'd say it's the forecast. Of course I see a relationship between budgets and forecasts. In a sense the forecast predicts the cash flow effects of the budget, including expected revenue.

But in his down home Huntsville Alabama way, he draws a sharper distinction, putting it like this: "A budget is a license to spend. A forecast is your roadmap to profitability."

There have been times when my clients didn't have budgets. I could never get them to sit down and finish one with me. Whenever that has happened I've done what he recommends: forecast into the future working with recent actuals.

No budget necessary. It's Lean. It works.

Eight: The Crabtree KPIs (Key Performance Indicators):

- Labor Efficiency (Gross Profit / Total Labor)

- Accounts Receivable DSO (Days Sales Outstanding). That's A/R divided by Average Daily Sales over, say, a recent two month period.

- Core Capital (2 months operating expenses in cash and no debt)

- Salary Cap vs. Actual Labor